A business is usually the most valuable asset; yet owners typically have no idea what their business is worth. Unlike real estate or brokerage investments, owners are handicapped by not having readily available information to indicate business worth.

A business is usually the most valuable asset; yet owners typically have no idea what their business is worth. Unlike real estate or brokerage investments, owners are handicapped by not having readily available information to indicate business worth.

For example, with real estate, nearby transactions occur daily. You can usually find that 4 bedroom, 2 bath home with similar square footage that recently sold within your neighborhood. You know how long it was on the market for and what is sold for.

By the same token, the stock exchange reflects the current values of publicly sold securities. A sale will result in cash received within days.

Unfortunately, privately held businesses are unique. They are not often sold. Transactions are not publicized. What’s more, your business and circumstances related to the sale may be different.

What is my business worth?

The underlying purpose of all businesses is to provide an income stream (cash flow) and/or appreciation in value.

Income

Using a “capitalized earnings” model is one method to measure income. This model uses historical information to determine value. Another way to measure cash flow is through a “discounted cash flow” model, which looks at what is expected to happen in the future. This method is best used when future results are expected to differ from historical results.

Measuring income (cash flow) goes beyond looking at the “net income” number on the income statement. Sometimes current accounting and tax treatment can skew reported income, making such income significantly different from cash flow. For instance some expenses, such as depreciation and amortization, have no impact on cash flow. Many experts look at “EBITDA” as a better measure to approximate cash flow. EBITDA is “Earnings Before Interest on debt, Taxes, Depreciation, and Amortization.” Others will also incorporate changes in the company’s balance sheet.

As an owner, you should be aware of all personal benefits that you get through the business. Such benefits may be viewed as “discretionary”. If the discretionary benefits can be transferred to a new owner, they could increase cash flow and increase value.

The income stream / cash flow needs to be capitalized or discounted, depending on methodology used. This process essentially assigns a risk factor to the cash flow. The higher the discount rate or capitalization rate, the higher the risk, and the lower the value.

You may have heard about people applying a multiplier, such as 4 times EBITDA, when determining a value of a business. In this example the multiplier is the inverse of a capitalization rate of 25 percent. If the capitalization rate was 20%, a multiplier of 5 times would be used. As these examples indicate, the lower the risk, the lower the capitalization rate. The lower the capitalization rate, the higher the multiplier, which leads to a higher value.

Factors that impact capitalization rates include the stability of the earnings, nature of the business and risks involved.

Net Assets

In most circumstances, net assets (which are assets less liabilities) represent a minimum value. The balance sheet may not reflect current market values. The assets should be examined to assess whether the company has “non-operating assets”. Such assets may be non-essential assets that are not used within the business.

The fair market value of non-operating assets are typically added to the cash flow. Sometimes, the underlying assets are more valuable than the current measured cash flow. A florist in Manhattan, who owns the flower shop real estate would likely sell her business to a buyer who is looking to re-purpose the real estate, resulting in the seller receiving a higher price.

Market Approach

The IRS emphasizes the importance of considering public company comparisons which have active, free trading market-to-value shares. However, finding such comparable public companies can be difficult. Appraisers also consider databases which may provide sufficient detail about a transaction related to a non-public acquisition. Comparability is challenging when using this approach. See our prior article on the Comparability Considerations for more information on this topic.

Understanding the Business

In order to accurately value a business, you need to understand the company. By understanding the company, you can better assess risk. It is helpful to understand your unique strengths, weaknesses, opportunities and threats. Understanding the competitive landscape and other factors that impact current and future operations impact risk. See our prior article on Understanding Risk for more information on this topic.

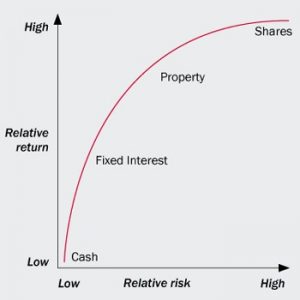

With all businesses, there is risk. From an investment prospective, a high-risk investment requires a high return.

Risk is often measured based upon investment alternatives. Here are some common examples.

An investor with cash can put money in a bank account with little risk; in return, he receives a very modest return.

As a riskier investment, an individual can put money into the stock market. With a stock market investment, an investor could easily lose money, but may hit a home run by acquiring a highly sought after stock which appreciates in value.

Inherently, investors require a higher return to invest in the stock market to account for the added risk. Likewise, a privately held business is more risky and requires a higher return.

Can I Increase the Value of My Company?

With proper planning, you can increase the value of your business. If you can take steps to lower company specific risk, you can make your company more valuable. Examples of proactive steps could include:

- Reduce reliance on key management / employee(s);

- Diversify products, services, customers, and suppliers;

- Optimize capital and operational structure (Do you have too much debt? Do you have sufficient working capital?);

- Increase margins by examining areas to reduce costs and improve the cash conversion cycle.

Different Values

It is important to note that Value(s) can differ based upon circumstances. Sometimes rules and laws (statutes) may define and interpret value differently. This is the case with financial reporting, gift and estate tax, divorce, bankruptcy, and other litigation.

“Fair Value” is used for financial reporting based upon accounting practices as established by the Financial Accounting Standards Board (FASB). It is typically defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (FASB Statement No. 157, 2007). This is the standard used for mergers and acquisitions, purchase/sales of businesses, and financial reporting (on GAAP financial statements).

“Fair Market Value” is the price, expressed in terms of cash equivalents, at which property would change hands between a hypothetical willing and able buyer and a hypothetical willing and able seller, acting at arms length in an open and unrestricted market, when neither is under compulsion to buy or sell and when both have reasonable knowledge of the relevant facts. This standard is used by the IRS (for estate & gift), and has been adopted as the standard in many litigation matters.

“Liquidation Value” is the net amount that would be realized if the business is terminated and the assets are sold piecemeal. Liquidation can be either “orderly” or “forced.”

Other factors may influence the standard of value. If you are able to sell the business to a competitor or to a supplier, my may be able to obtain a higher price, as the buyer may gain some strategic or synergistic advantages with the consummated sale.

If you are interested in finding out what your business is worth, or you want more about the valuation process, please contact us for a free consultation.